Key market movements for the quarter

Shares and bonds across the board were under pressure in the second quarter of 2022, as markets priced in further increases in interest rates as well as an increased risk of recession. Amongst equities returns, which were generally poor, the MSCI World Value index significantly outperformed its Growth counterpart, although both registered double-digit declines. The Chinese share market provided a rare highlight as prolonged lockdowns were lifted in some major cities, allowing macroeconomic indicators there to show some improvement.

Inflation rates in major economies continued to persist at multi-decade highs, with various central banks raising interest rates and others clearly signalling their intention to do so soon. The quarter also saw mounting concerns over global economic growth prospects, with the fight to tame inflation likely to result in monetary policy settings that would be less supportive than the global economy has enjoyed in recent years.

The potential for economies to experience a recession later this year became more widely contemplated and, towards the end of the quarter, economic indicators began to reflect a general moderating or slowing in economic activity.

International shares

In the US, investor focus was on inflation and the policy response from the US Federal Reserve. The bank enacted initial rate hikes during the quarter and signalled that there would be more to come. Even so, they admitted the task of bringing inflation down without triggering a recession would be a challenging balancing act.

While weak sentiment affected all sectors, consumer staples and utilities companies were comparatively resilient. However, there were some dramatic declines for some companies, most notably in the media, entertainment and auto sectors.

Further steep declines were common for eurozone shares, as the war in Ukraine continued and concerns mounted over potential gas shortages, with supplies to Germany a particular being a point of concern. Higher inflation also dented consumer confidence, with the European Central Bank (ECB) poised to raise interest rates in July.

UK equities also fell over the quarter, with economically sensitive areas of the market performing poorly towards the end of the period amidst rising recessionary risks.

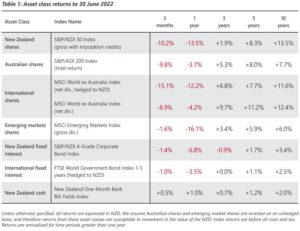

In New Zealand dollar terms, the MSCI World ex-Australia Index delivered a quarterly return of -15.1% on a hedged basis and -6.9% unhedged. This meant the rolling 12 month return for the New Zealand dollar hedged index reduced to -12.2% while the unhedged index is down -4.2%.

Source: MSCI World ex-Australia Index (net div.)

Emerging markets shares

In a quarter where global share markets generally slumped, it was somewhat against the usual trend to see the relative outperformance of the emerging markets region (as a whole). When investors are wary of exposure to higher risk assets, emerging markets are often harder hit. But not this quarter.

That said, plenty of emerging market share markets did post declines. The South Korea share market struggled, with financials, technology and energy stocks hit particularly hard amid growing fears of a global recession. Taiwan was also significantly lower, on fears that rising inflation and global supply chain problems would weaken demand for its technology products.

The Latin American markets of Colombia, Peru and Brazil were amongst the weakest in the MSCI Emerging Markets Index. A combination of rising concerns about a global recession, domestic policy uncertainty and weaker industrial metals prices later in the quarter, all contributed to the declines.

The emerging European markets of Poland and Hungary both underperformed by a wide margin, as geopolitical risks stemming from Russia’s invasion of neighbouring Ukraine persisted.

The shining light for the region was China which managed to deliver a solid positive return for the quarter. With lockdown measures in certain Chinese cities being eased, this prompted a recovery in economic activity.

As the largest constituent in the emerging markets region, China’s positive result was a major driver to the mild loss for this asset class in the quarter, with the MSCI Emerging Markets Index producing a quarterly return of -1.6% in unhedged New Zealand dollar terms.

Source: MSCI Emerging Markets Index (gross div.)

New Zealand shares

The New Zealand market endured a difficult quarter with the S&P/NZX 50 Index returning -10.2%. Whilst at the individual company level there was ‘red ink’ almost across the board for the quarter, it was the industrials and health care sectors that contributed the largest drag on the performance of the index.

The two worst affected firms in the industrials sector, Air New Zealand and Freightways were down -27.9% and -25.9% respectively for the quarter, as the prospect of weaker economic growth weighed heavily on their prices. While building materials firm Fletcher Building fell -21.0% as sentiment around the domestic building and construction sector continued to cool.

With only six firms in the top 50 delivering a positive return in the quarter, it was software firm Pushpay that enjoyed the strongest performance, gaining 11.4%. This followed news that two existing shareholders (BGH Capital and Sixth Street) were intending to make a takeover bid for the firm.

Source: S&P/NZX 50 Index (gross with imputation credits)

Australian shares

The Australian share market (ASX 200 Total Return Index) had a similarly tough time sliding -11.9% over the quarter in local currency terms. Returns to unhedged New Zealand investors were slightly better at -9.8%, due to an appreciation in the value of the Australian dollar over the quarter.

Once again, the dispersion in sectoral returns was a feature of the market, with the utilities and energy sectors standing apart from the rest by delivering small gains. At the other end of the spectrum, the information technology sector suffered a very poor quarter as growth company valuations came under increasing pressure due to the expectation of faster rate hikes. The real estate and materials sectors were also very weak.

With only a little over one in ten companies in the ASX 200 delivering positive returns during the quarter, infrastructure firm Atlas Arteria (+23.1%) and small energy company Viva Energy Group (+23.0%) were the clear standouts.

At the other end of the standings, there were 21 companies within the ASX 200 that delivered returns of -35% or worse for the quarter. This list was littered with small capitalisation firms in the technology and basic materials sectors, as valuation concerns and general negative sentiment during the quarter impacted these companies the most.

Source: S&P/ASX 200 Index (total return)

International fixed interest

Global bonds saw their prices continue to decline during the quarter, with yields markedly higher due to elevated inflation data, increasingly ‘hawkish’ central bank statements and rising interest rates. There was a small bond rally (price gains) towards the end of the quarter as economic growth concerns began to rise.

With inflation data in major economies at multi-decade highs, the quarter was characterised by various central banks raising interest rates and others signalling their intention to do so. The quarter also saw mounting concerns over future economic growth prospects, including the possibility of a recession later this year.

In the US, the Federal Reserve implemented a series of interest rate hikes, raising the US policy rate by 0.50% in May and a further 0.75% in June, their largest single rate hike since 1994. At the same time, Federal officials cut their 2022 growth forecasts. In response, the US 10 year bond yield rose from 2.35% to 3.02% over the quarter.

European bond yields were volatile as the European central bank indicated it would end asset purchases early in the third quarter and raise interest rates soon after. With this backdrop, the German 10 year bond yield increased from 0.55% to 1.37% over the quarter.

In the UK, the Bank of England implemented further interest rate hikes, bringing the total to five in the current cycle, as well as raising its inflation forecast to a staggering 11%. This helped push the UK 10 year bond yield up from 1.61% to 2.24%.

Corporate bonds also suffered in the broad bond market sell off, and generally underperformed government bonds as credit spreads widened markedly. With mounting concerns over the economic outlook, high yield credit securities (i.e lower credit quality) were hit particularly hard.

The FTSE World Government Bond Index 1-5 Years (hedged to NZD) returned -1.0% for the quarter, while the broader Bloomberg Global Aggregate Bond Index (hedged to NZD) returned -4.5%.

Source: FTSE World Government Bond Index 1-5 Years (hedged to NZD)

New Zealand fixed interest

The Reserve Bank of New Zealand (RBNZ) elected to increase the Official Cash Rate (OCR) by a further 0.50% on 14 April and again by another 0.50% on 26 May, taking this benchmark rate from 1.00% to 2.00% by the end of the quarter.

In its accompanying statement, the RBNZ noted that “the level of global economic activity is generating rising inflation pressures that are being exacerbated by ongoing supply disruptions driven by both Covid-19 persistence and the Russian invasion of Ukraine. The latter continues to cause very high prices for food and energy commodities.”

The Monetary Policy Committee also reconfirmed it planned to continue to lift the OCR “at pace” to a level that will confidently bring consumer price inflation to within its 1-3% target range.

In effect, this confirms the expectations of the RBNZ are for interest rates to continue to rise, for the time being at least. Given this outlook, the New Zealand 10 year government bond yield climbed from 3.25% at the end of the first quarter to 3.87% at the end of June. The New Zealand 2 year government bond yield followed an entirely similar pattern, beginning the quarter at 2.92% and ending the June quarter at 3.51%, a yield increase of 0.59%. Similar to the effects seen overseas, these rising bond yields generally resulted in negative short term returns for bonds of all durations.

The S&P/NZX A-Grade Corporate Bond Index fell -1.4% for the quarter, while the longer duration but higher quality S&P/NZX NZ Government Bond Index fell -3.2%.

Source: S&P/NZX A-Grade Corporate Bond Index